The New Era of Life Sciences Will Be Won on Forecasting Excellence

The New Era of Life Sciences Will Be Won on Forecasting Excellence

In this article, we explore why the blockbuster era is giving way to a more fragmented, competitive landscape - and how machine learning is changing the way life science companies predict erosion, time investments, and launch with precision.

Loss of exclusivity is accelerating across major therapeutic areas, pushing many companies toward an imminent patent cliff and forcing more deliberate and data-driven end-of-lifecycle planning. At the same time, true commercial white space is becoming harder to find, and new launches are increasingly smaller, more segmented, and more competitive.

The result is a reality where planning must be more dynamic, trade-offs more explicit, and commercial execution tightly linked to evolving market signals.

This POV covers two connected challenges facing life sciences today:

(1) How to predict and manage the impact of loss of exclusivity (LoE) under highly variable erosion dynamics - including when to invest further versus accept fast erosion.

(2) How to plan, launch, and scale new assets in a world of smaller, more fragmented opportunities, where early forecasting errors can permanently cap value

Across both, machine-learning-based forecasting and scenario modeling are becoming core operating capabilities of modern life sciences- not as reporting tools, but as systems through which future outcomes are predicted, tested, and acted upon.

Loss of exclusivity is accelerating across major therapeutic areas, pushing many companies toward an imminent patent cliff and forcing more deliberate and data-driven end-of-lifecycle planning. At the same time, true commercial white space is becoming harder to find, and new launches are increasingly smaller, more segmented, and more competitive.

The result is a reality where planning must be more dynamic, trade-offs more explicit, and commercial execution tightly linked to evolving market signals.

This POV covers two connected challenges facing life sciences today:

(1) How to predict and manage the impact of loss of exclusivity (LoE) under highly variable erosion dynamics - including when to invest further versus accept fast erosion.

(2) How to plan, launch, and scale new assets in a world of smaller, more fragmented opportunities, where early forecasting errors can permanently cap value

Across both, machine-learning-based forecasting and scenario modeling are becoming core operating capabilities of modern life sciences- not as reporting tools, but as systems through which future outcomes are predicted, tested, and acted upon.

Loss of exclusivity is accelerating across major therapeutic areas, pushing many companies toward an imminent patent cliff and forcing more deliberate and data-driven end-of-lifecycle planning. At the same time, true commercial white space is becoming harder to find, and new launches are increasingly smaller, more segmented, and more competitive.

The result is a reality where planning must be more dynamic, trade-offs more explicit, and commercial execution tightly linked to evolving market signals.

This POV covers two connected challenges facing life sciences today:

(1) How to predict and manage the impact of loss of exclusivity (LoE) under highly variable erosion dynamics - including when to invest further versus accept fast erosion.

(2) How to plan, launch, and scale new assets in a world of smaller, more fragmented opportunities, where early forecasting errors can permanently cap value

Across both, machine-learning-based forecasting and scenario modeling are becoming core operating capabilities of modern life sciences- not as reporting tools, but as systems through which future outcomes are predicted, tested, and acted upon.

The life science industry is facing two forecasting problems at once

Loss of exclusivity is accelerating across major therapeutic areas, pushing many companies toward an imminent patent cliff and forcing more deliberate and data-driven end-of-lifecycle planning. At the same time, true commercial white space is becoming harder to find, and new launches are increasingly smaller, more segmented, and more competitive.

The result is a reality where planning must be more dynamic, trade-offs more explicit, and commercial execution tightly linked to evolving market signals.

This POV covers two connected challenges facing life sciences today:

(1) How to predict and manage the impact of loss of exclusivity (LoE) under highly variable erosion dynamics - including when to invest further versus accept fast erosion.

(2) How to plan, launch, and scale new assets in a world of smaller, more fragmented opportunities, where early forecasting errors can permanently cap value

Across both, machine-learning-based forecasting and scenario modeling are becoming core operating capabilities of modern life sciences- not as reporting tools, but as systems through which future outcomes are predicted, tested, and acted upon.

The life science industry is facing two forecasting problems at once

Loss of exclusivity is accelerating across major therapeutic areas, pushing many companies toward an imminent patent cliff and forcing more deliberate and data-driven end-of-lifecycle planning. At the same time, true commercial white space is becoming harder to find, and new launches are increasingly smaller, more segmented, and more competitive.

The result is a reality where planning must be more dynamic, trade-offs more explicit, and commercial execution tightly linked to evolving market signals.

This POV covers two connected challenges facing life sciences today:

(1) How to predict and manage the impact of loss of exclusivity (LoE) under highly variable erosion dynamics - including when to invest further versus accept fast erosion.

(2) How to plan, launch, and scale new assets in a world of smaller, more fragmented opportunities, where early forecasting errors can permanently cap value

Across both, machine-learning-based forecasting and scenario modeling are becoming core operating capabilities of modern life sciences- not as reporting tools, but as systems through which future outcomes are predicted, tested, and acted upon.

The life science industry is facing two forecasting problems at once

In life science, much of portfolio strategy is still implicitly anchored to the pursuit of the next “blockbuster” - typically defined as a medicine generating at least USD 1 billion in annual global revenue. That ambition was shaped by an industry context in which achieving and sustaining blockbuster-scale revenues was both realistic and repeatable.

For decades, the life science industry operated under a relatively stable set of assumptions:

- Large, under-treated, high–unmet-need disease populations

- Few competitors per mechanism

- Broad molecules with multi-indication potential

- Long periods of economically defensible exclusivity

In that environment, the blockbuster model worked. Assets like Keytruda, which expanded rapidly across tumor types within the PD-1/PD-L1 class, could support multiple indications, justify large commercial organizations, and deliver (relatively) predictable, concentrated revenue over a decade or more. Planning and forecasting were comparatively straightforward: demand curves were smoother, competitive threats fewer, and execution largely about scale and speed. That model has not disappeared entirely - but the conditions that sustained it are becoming less common.

In life science, much of portfolio strategy is still implicitly anchored to the pursuit of the next “blockbuster” - typically defined as a medicine generating at least USD 1 billion in annual global revenue. That ambition was shaped by an industry context in which achieving and sustaining blockbuster-scale revenues was both realistic and repeatable.

For decades, the life science industry operated under a relatively stable set of assumptions:

- Large, under-treated, high–unmet-need disease populations

- Few competitors per mechanism

- Broad molecules with multi-indication potential

- Long periods of economically defensible exclusivity

In that environment, the blockbuster model worked. Assets like Keytruda, which expanded rapidly across tumor types within the PD-1/PD-L1 class, could support multiple indications, justify large commercial organizations, and deliver (relatively) predictable, concentrated revenue over a decade or more. Planning and forecasting were comparatively straightforward: demand curves were smoother, competitive threats fewer, and execution largely about scale and speed. That model has not disappeared entirely - but the conditions that sustained it are becoming less common.

In life science, much of portfolio strategy is still implicitly anchored to the pursuit of the next “blockbuster” - typically defined as a medicine generating at least USD 1 billion in annual global revenue. That ambition was shaped by an industry context in which achieving and sustaining blockbuster-scale revenues was both realistic and repeatable.

For decades, the life science industry operated under a relatively stable set of assumptions:

- Large, under-treated, high–unmet-need disease populations

- Few competitors per mechanism

- Broad molecules with multi-indication potential

- Long periods of economically defensible exclusivity

In that environment, the blockbuster model worked. Assets like Keytruda, which expanded rapidly across tumor types within the PD-1/PD-L1 class, could support multiple indications, justify large commercial organizations, and deliver (relatively) predictable, concentrated revenue over a decade or more. Planning and forecasting were comparatively straightforward: demand curves were smoother, competitive threats fewer, and execution largely about scale and speed. That model has not disappeared entirely - but the conditions that sustained it are becoming less common.

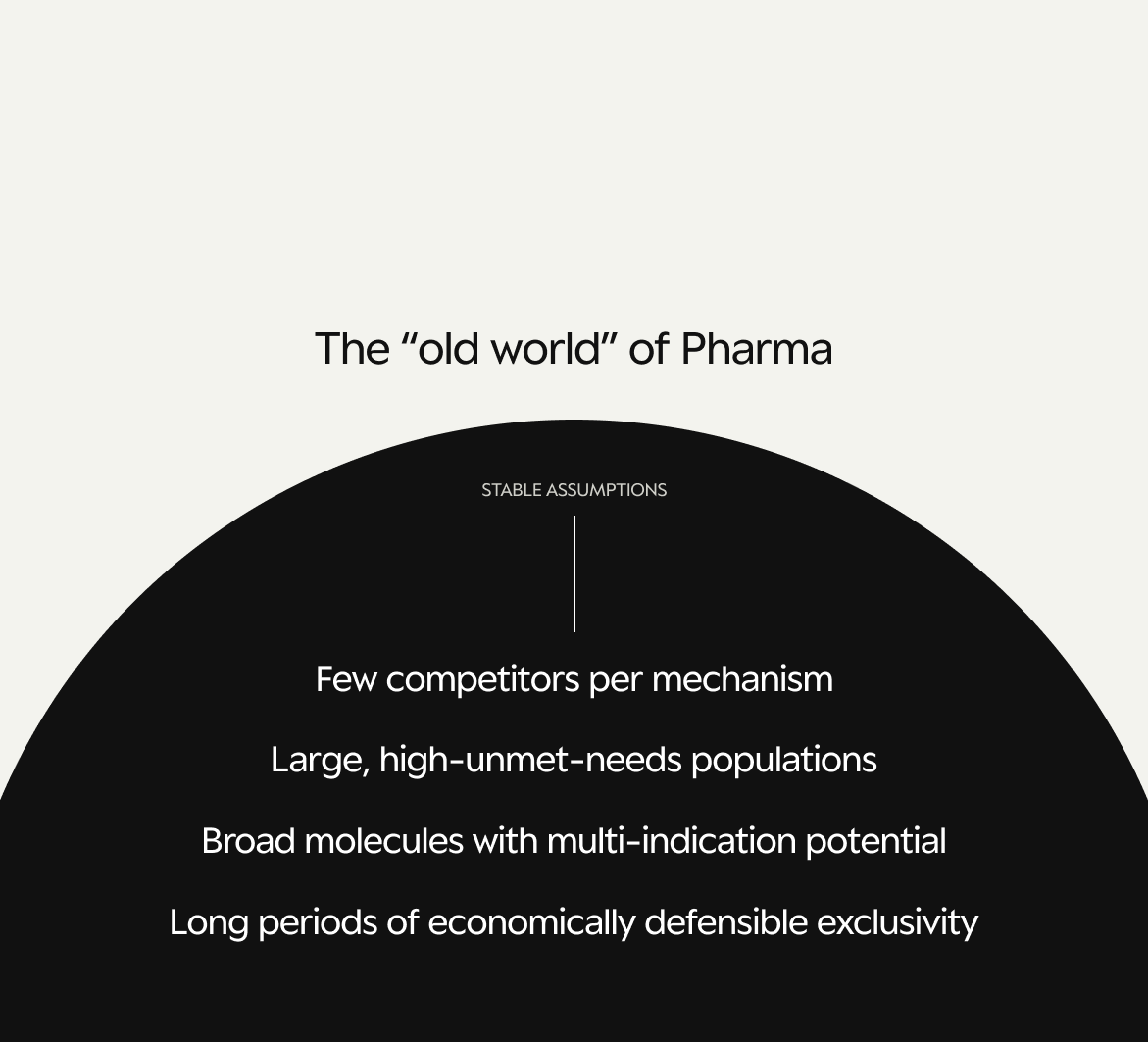

Blockbuster were built on assumptions that are fading

In life science, much of portfolio strategy is still implicitly anchored to the pursuit of the next “blockbuster” - typically defined as a medicine generating at least USD 1 billion in annual global revenue. That ambition was shaped by an industry context in which achieving and sustaining blockbuster-scale revenues was both realistic and repeatable.

For decades, the life science industry operated under a relatively stable set of assumptions:

- Large, under-treated, high–unmet-need disease populations

- Few competitors per mechanism

- Broad molecules with multi-indication potential

- Long periods of economically defensible exclusivity

In that environment, the blockbuster model worked. Assets like Keytruda, which expanded rapidly across tumor types within the PD-1/PD-L1 class, could support multiple indications, justify large commercial organizations, and deliver (relatively) predictable, concentrated revenue over a decade or more. Planning and forecasting were comparatively straightforward: demand curves were smoother, competitive threats fewer, and execution largely about scale and speed. That model has not disappeared entirely - but the conditions that sustained it are becoming less common.

Blockbuster were built on assumptions that are fading

In life science, much of portfolio strategy is still implicitly anchored to the pursuit of the next “blockbuster” - typically defined as a medicine generating at least USD 1 billion in annual global revenue. That ambition was shaped by an industry context in which achieving and sustaining blockbuster-scale revenues was both realistic and repeatable.

For decades, the life science industry operated under a relatively stable set of assumptions:

- Large, under-treated, high–unmet-need disease populations

- Few competitors per mechanism

- Broad molecules with multi-indication potential

- Long periods of economically defensible exclusivity

In that environment, the blockbuster model worked. Assets like Keytruda, which expanded rapidly across tumor types within the PD-1/PD-L1 class, could support multiple indications, justify large commercial organizations, and deliver (relatively) predictable, concentrated revenue over a decade or more. Planning and forecasting were comparatively straightforward: demand curves were smoother, competitive threats fewer, and execution largely about scale and speed. That model has not disappeared entirely - but the conditions that sustained it are becoming less common.

Blockbuster were built on assumptions that are fading

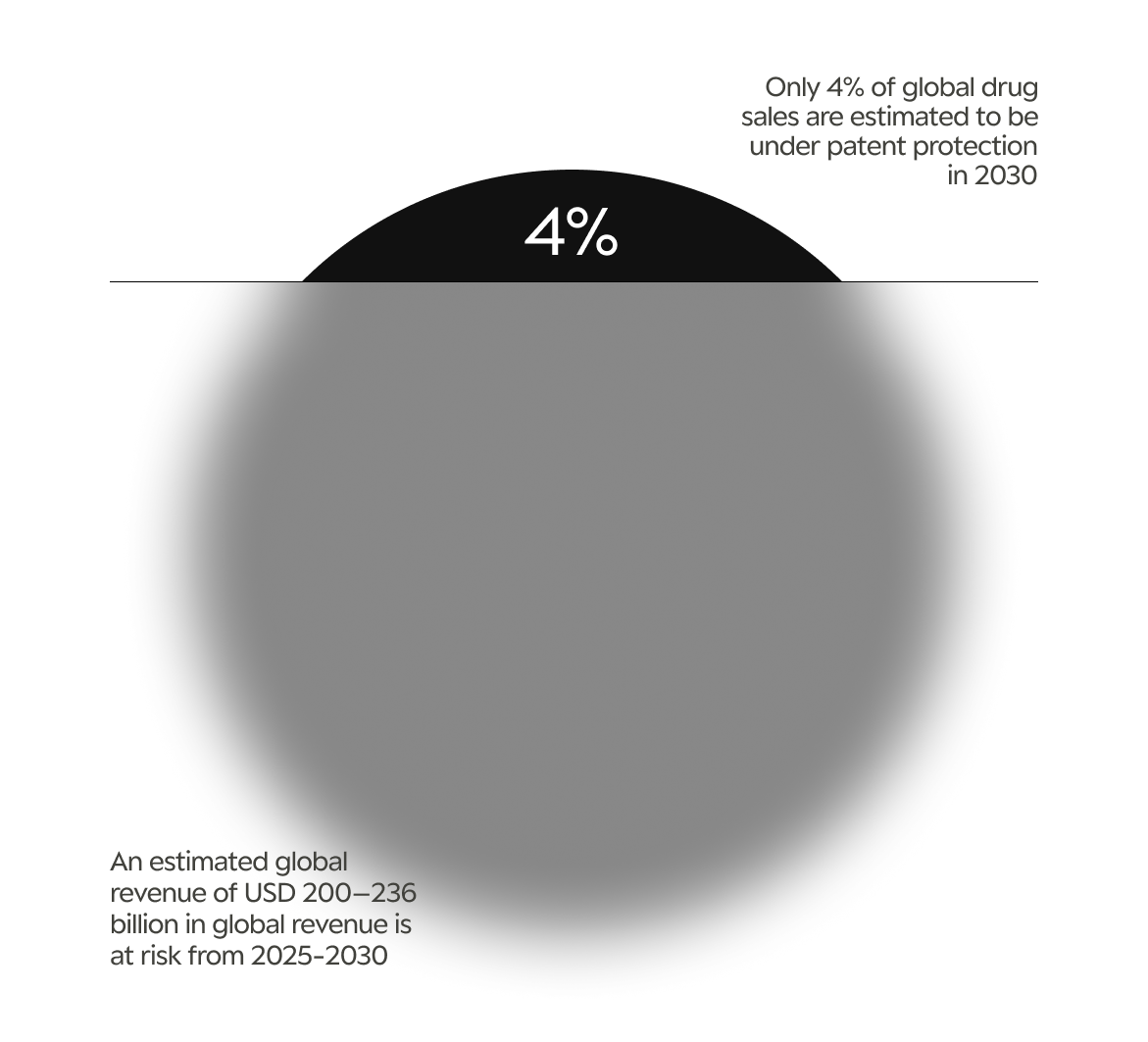

Loss of exclusivity as a structural pressure

Unlike earlier patent cliffs, this pressure is not concentrated in a single year or therapeutic area. Oncology, immunology, cardiovascular disease, and diabetes are all heavily affected. At the same time, payer dynamics, generic & biosimilar uptake, and competitive sequencing vary widely by market and therapy area, making erosion patterns more heterogeneous and harder to model with confidence.

In practice, this means that LoE is no longer a contained forecasting event with a small number of standard assumptions. It has become a prolonged period of elevated uncertainty that directly shapes portfolio, resourcing, and investment decisions.

Narrowing White Space

At the same time, the scientific and competitive landscape has matured:

- Many major diseases now have multiple approved mechanisms

- Pipelines are crowded with second- and third-in-class assets

- Differentiation is often incremental rather than transformative

While blockbuster opportunities still exist - particularly in large unmet needs such as Alzheimer’s or Parkinson’s, or through multi-indication strategies (for example C5 inhibition) - the typical launch today targets a smaller, more tightly defined population, often under specific biomarker, line-of-therapy, or access constraints. Take for example a disease like NASH, multiple assets across different mechanisms have reached late-stage development in parallel and are launching within a narrow window, fragmenting what was once viewed as a single blockbuster opportunity.

The net effect is a shift away from a small number of dominant assets toward broader portfolios of more specialized medicines.

Loss of exclusivity as a structural pressure

Unlike earlier patent cliffs, this pressure is not concentrated in a single year or therapeutic area. Oncology, immunology, cardiovascular disease, and diabetes are all heavily affected. At the same time, payer dynamics, generic & biosimilar uptake, and competitive sequencing vary widely by market and therapy area, making erosion patterns more heterogeneous and harder to model with confidence.

In practice, this means that LoE is no longer a contained forecasting event with a small number of standard assumptions. It has become a prolonged period of elevated uncertainty that directly shapes portfolio, resourcing, and investment decisions.

Narrowing White Space

At the same time, the scientific and competitive landscape has matured:

- Many major diseases now have multiple approved mechanisms

- Pipelines are crowded with second- and third-in-class assets

- Differentiation is often incremental rather than transformative

While blockbuster opportunities still exist - particularly in large unmet needs such as Alzheimer’s or Parkinson’s, or through multi-indication strategies (for example C5 inhibition) - the typical launch today targets a smaller, more tightly defined population, often under specific biomarker, line-of-therapy, or access constraints. Take for example a disease like NASH, multiple assets across different mechanisms have reached late-stage development in parallel and are launching within a narrow window, fragmenting what was once viewed as a single blockbuster opportunity.

The net effect is a shift away from a small number of dominant assets toward broader portfolios of more specialized medicines.

Loss of exclusivity as a structural pressure

Unlike earlier patent cliffs, this pressure is not concentrated in a single year or therapeutic area. Oncology, immunology, cardiovascular disease, and diabetes are all heavily affected. At the same time, payer dynamics, generic & biosimilar uptake, and competitive sequencing vary widely by market and therapy area, making erosion patterns more heterogeneous and harder to model with confidence.

In practice, this means that LoE is no longer a contained forecasting event with a small number of standard assumptions. It has become a prolonged period of elevated uncertainty that directly shapes portfolio, resourcing, and investment decisions.

Narrowing White Space

At the same time, the scientific and competitive landscape has matured:

- Many major diseases now have multiple approved mechanisms

- Pipelines are crowded with second- and third-in-class assets

- Differentiation is often incremental rather than transformative

While blockbuster opportunities still exist - particularly in large unmet needs such as Alzheimer’s or Parkinson’s, or through multi-indication strategies (for example C5 inhibition) - the typical launch today targets a smaller, more tightly defined population, often under specific biomarker, line-of-therapy, or access constraints. Take for example a disease like NASH, multiple assets across different mechanisms have reached late-stage development in parallel and are launching within a narrow window, fragmenting what was once viewed as a single blockbuster opportunity.

The net effect is a shift away from a small number of dominant assets toward broader portfolios of more specialized medicines.

The world of life sciences is changing

Loss of exclusivity as a structural pressure

Unlike earlier patent cliffs, this pressure is not concentrated in a single year or therapeutic area. Oncology, immunology, cardiovascular disease, and diabetes are all heavily affected. At the same time, payer dynamics, generic & biosimilar uptake, and competitive sequencing vary widely by market and therapy area, making erosion patterns more heterogeneous and harder to model with confidence.

In practice, this means that LoE is no longer a contained forecasting event with a small number of standard assumptions. It has become a prolonged period of elevated uncertainty that directly shapes portfolio, resourcing, and investment decisions.

Narrowing White Space

At the same time, the scientific and competitive landscape has matured:

- Many major diseases now have multiple approved mechanisms

- Pipelines are crowded with second- and third-in-class assets

- Differentiation is often incremental rather than transformative

While blockbuster opportunities still exist - particularly in large unmet needs such as Alzheimer’s or Parkinson’s, or through multi-indication strategies (for example C5 inhibition) - the typical launch today targets a smaller, more tightly defined population, often under specific biomarker, line-of-therapy, or access constraints. Take for example a disease like NASH, multiple assets across different mechanisms have reached late-stage development in parallel and are launching within a narrow window, fragmenting what was once viewed as a single blockbuster opportunity.

The net effect is a shift away from a small number of dominant assets toward broader portfolios of more specialized medicines.

The world of life sciences is changing

Loss of exclusivity as a structural pressure

Unlike earlier patent cliffs, this pressure is not concentrated in a single year or therapeutic area. Oncology, immunology, cardiovascular disease, and diabetes are all heavily affected. At the same time, payer dynamics, generic & biosimilar uptake, and competitive sequencing vary widely by market and therapy area, making erosion patterns more heterogeneous and harder to model with confidence.

In practice, this means that LoE is no longer a contained forecasting event with a small number of standard assumptions. It has become a prolonged period of elevated uncertainty that directly shapes portfolio, resourcing, and investment decisions.

Narrowing White Space

At the same time, the scientific and competitive landscape has matured:

- Many major diseases now have multiple approved mechanisms

- Pipelines are crowded with second- and third-in-class assets

- Differentiation is often incremental rather than transformative

While blockbuster opportunities still exist - particularly in large unmet needs such as Alzheimer’s or Parkinson’s, or through multi-indication strategies (for example C5 inhibition) - the typical launch today targets a smaller, more tightly defined population, often under specific biomarker, line-of-therapy, or access constraints. Take for example a disease like NASH, multiple assets across different mechanisms have reached late-stage development in parallel and are launching within a narrow window, fragmenting what was once viewed as a single blockbuster opportunity.

The net effect is a shift away from a small number of dominant assets toward broader portfolios of more specialized medicines.

The world of life sciences is changing

This environment creates two closely linked challenges:

- Predicting LoE erosion accurately enough to time investment and exit decision

- Forecasting launch trajectories accurately enough to resource them appropriately

These are often treated separately. In reality, they are two sides of the same forecasting problem: how to allocate investment and resources effectively

This environment creates two closely linked challenges:

- Predicting LoE erosion accurately enough to time investment and exit decision

- Forecasting launch trajectories accurately enough to resource them appropriately

These are often treated separately. In reality, they are two sides of the same forecasting problem: how to allocate investment and resources effectively

This environment creates two closely linked challenges:

- Predicting LoE erosion accurately enough to time investment and exit decision

- Forecasting launch trajectories accurately enough to resource them appropriately

These are often treated separately. In reality, they are two sides of the same forecasting problem: how to allocate investment and resources effectively

Two sides of the same forecasting problem

This environment creates two closely linked challenges:

- Predicting LoE erosion accurately enough to time investment and exit decision

- Forecasting launch trajectories accurately enough to resource them appropriately

These are often treated separately. In reality, they are two sides of the same forecasting problem: how to allocate investment and resources effectively

Two sides of the same forecasting problem

This environment creates two closely linked challenges:

- Predicting LoE erosion accurately enough to time investment and exit decision

- Forecasting launch trajectories accurately enough to resource them appropriately

These are often treated separately. In reality, they are two sides of the same forecasting problem: how to allocate investment and resources effectively

Two sides of the same forecasting problem

Historically, LoE planning relied on a limited set of simplified assumptions: expected generic or biosimilar entry, an average erosion curve from a small set of previous analogues, and annual planning cycles. Those assumptions were imperfect, but no better alternatives existed.

In today’s heterogeneous environment, this assumption-based approach breaks down.

Erosion varies significantly based on:

- Market-specific Gx / BSM substitution rules

- Channel dynamics

- Product characteristics

- Disease area dynamics & patient/prescriber behavior

- Competitive factors and pricing

ML-Based Forecasting as the New LoE Decision-Making Tool

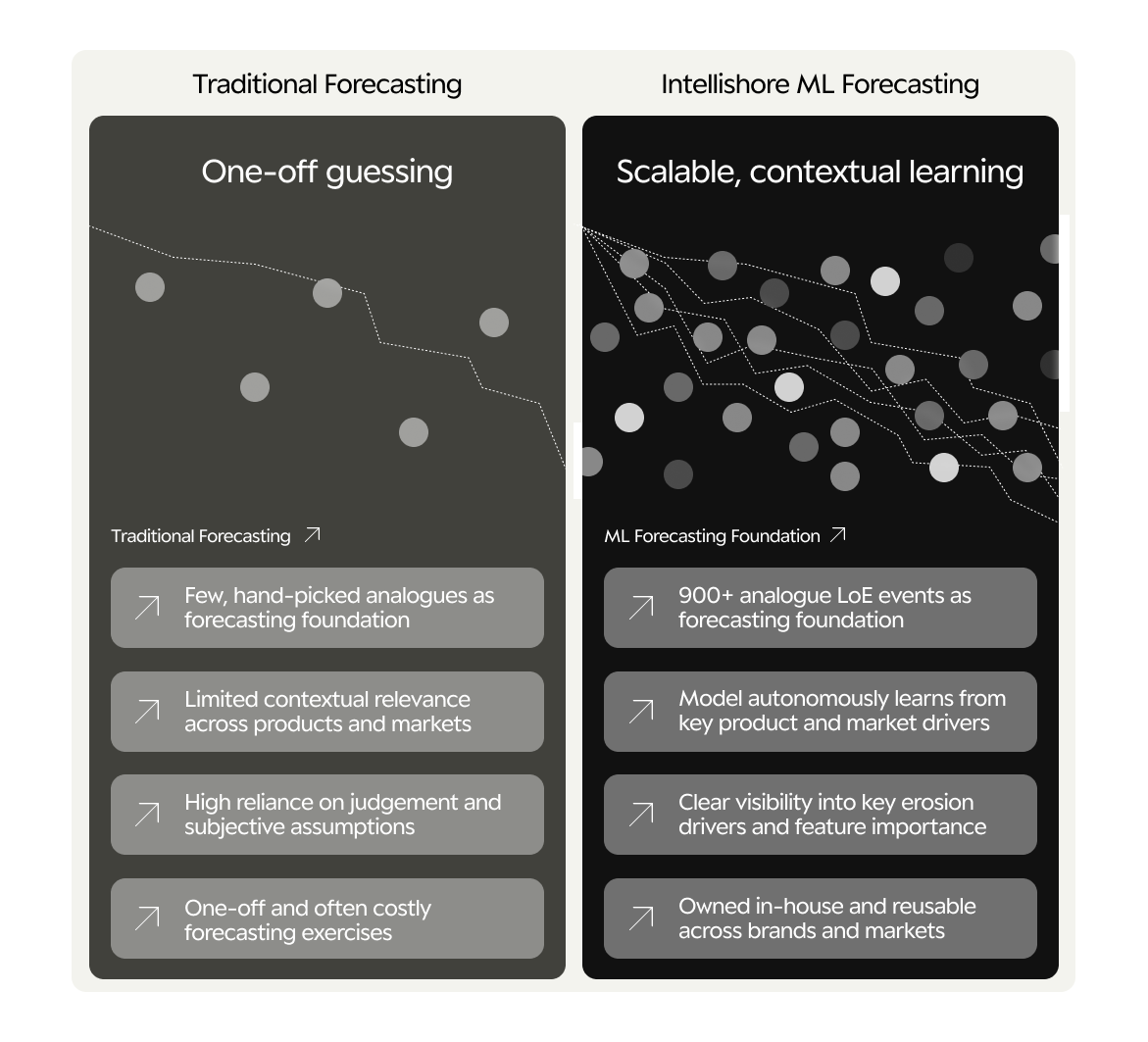

Machine learning changes how LoE can be managed by moving beyond one-off, assumption-driven projections toward data-driven, adaptive forecasting. Rather than relying on a small set of manually selected analogues and their past erosion curves, ML-based models learn from thousands of analogue characteristics across hundreds of assets and markets based on e.g., IQVIA Midas data.

In practice these ML-based models can:

- Learn from past LOE erosion observations - across therapy areas, products and markets

- Account for both product and market-specific characteristics and learn from thousands of different feature combinations to accurately develop a unique erosion prediction for the target being forecasted

- Dynamically update forecasts as new competitors enter or other market conditions change

- Provide insights on the most influential features for a given erosion forecast – allowing decision-makers to see whether e.g., price, commercial activity, Gx/BSM manufacturer historical aggressiveness, or market substitution enforcement is the most influential factor driving expectations

These models can be used to generate predictions for different strategic scenarios – e.g., allowing users to input different pricing scenarios and using that to predict expected volume. Additionally, they rely on no human assumptions as they automatically re-calculate product and market features based on objective data every month or quarter. These characteristics mean that leadership teams can be more agile and link forecasts directly to decisions on resource deployment, brand defense, and reinvestment timing.

In practice, this means that companies are better equipped to anticipate LOE impact and plan optimal strategic responses.

Scenario Modeling for Capital Reallocation

Forecasts only create value when they are tied to explicit decisions. Scenario modeling allows companies to test how different model inputs translate into different erosion curves and the associated trade-offs. Scenario modeling enables companies to explore questions such as:

- Which geographies remain economically defensible post-LoE?

- When do continued investments stop generating incremental returns?

- What post-LOE price strategy results in the best commercial outcome?

These insights ultimately help companies optimize capital allocation decisions and how to best redirect investments from low-potential LOE markets towards new or early-stage assets.

Historically, LoE planning relied on a limited set of simplified assumptions: expected generic or biosimilar entry, an average erosion curve from a small set of previous analogues, and annual planning cycles. Those assumptions were imperfect, but no better alternatives existed.

In today’s heterogeneous environment, this assumption-based approach breaks down.

Erosion varies significantly based on:

- Market-specific Gx / BSM substitution rules

- Channel dynamics

- Product characteristics

- Disease area dynamics & patient/prescriber behavior

- Competitive factors and pricing

ML-Based Forecasting as the New LoE Decision-Making Tool

Machine learning changes how LoE can be managed by moving beyond one-off, assumption-driven projections toward data-driven, adaptive forecasting. Rather than relying on a small set of manually selected analogues and their past erosion curves, ML-based models learn from thousands of analogue characteristics across hundreds of assets and markets based on e.g., IQVIA Midas data.

In practice these ML-based models can:

- Learn from past LOE erosion observations - across therapy areas, products and markets

- Account for both product and market-specific characteristics and learn from thousands of different feature combinations to accurately develop a unique erosion prediction for the target being forecasted

- Dynamically update forecasts as new competitors enter or other market conditions change

- Provide insights on the most influential features for a given erosion forecast – allowing decision-makers to see whether e.g., price, commercial activity, Gx/BSM manufacturer historical aggressiveness, or market substitution enforcement is the most influential factor driving expectations

These models can be used to generate predictions for different strategic scenarios – e.g., allowing users to input different pricing scenarios and using that to predict expected volume. Additionally, they rely on no human assumptions as they automatically re-calculate product and market features based on objective data every month or quarter. These characteristics mean that leadership teams can be more agile and link forecasts directly to decisions on resource deployment, brand defense, and reinvestment timing.

In practice, this means that companies are better equipped to anticipate LOE impact and plan optimal strategic responses.

Scenario Modeling for Capital Reallocation

Forecasts only create value when they are tied to explicit decisions. Scenario modeling allows companies to test how different model inputs translate into different erosion curves and the associated trade-offs. Scenario modeling enables companies to explore questions such as:

- Which geographies remain economically defensible post-LoE?

- When do continued investments stop generating incremental returns?

- What post-LOE price strategy results in the best commercial outcome?

These insights ultimately help companies optimize capital allocation decisions and how to best redirect investments from low-potential LOE markets towards new or early-stage assets.

Historically, LoE planning relied on a limited set of simplified assumptions: expected generic or biosimilar entry, an average erosion curve from a small set of previous analogues, and annual planning cycles. Those assumptions were imperfect, but no better alternatives existed.

In today’s heterogeneous environment, this assumption-based approach breaks down.

Erosion varies significantly based on:

- Market-specific Gx / BSM substitution rules

- Channel dynamics

- Product characteristics

- Disease area dynamics & patient/prescriber behavior

- Competitive factors and pricing

ML-Based Forecasting as the New LoE Decision-Making Tool

Machine learning changes how LoE can be managed by moving beyond one-off, assumption-driven projections toward data-driven, adaptive forecasting. Rather than relying on a small set of manually selected analogues and their past erosion curves, ML-based models learn from thousands of analogue characteristics across hundreds of assets and markets based on e.g., IQVIA Midas data.

In practice these ML-based models can:

- Learn from past LOE erosion observations - across therapy areas, products and markets

- Account for both product and market-specific characteristics and learn from thousands of different feature combinations to accurately develop a unique erosion prediction for the target being forecasted

- Dynamically update forecasts as new competitors enter or other market conditions change

- Provide insights on the most influential features for a given erosion forecast – allowing decision-makers to see whether e.g., price, commercial activity, Gx/BSM manufacturer historical aggressiveness, or market substitution enforcement is the most influential factor driving expectations

These models can be used to generate predictions for different strategic scenarios – e.g., allowing users to input different pricing scenarios and using that to predict expected volume. Additionally, they rely on no human assumptions as they automatically re-calculate product and market features based on objective data every month or quarter. These characteristics mean that leadership teams can be more agile and link forecasts directly to decisions on resource deployment, brand defense, and reinvestment timing.

In practice, this means that companies are better equipped to anticipate LOE impact and plan optimal strategic responses.

Scenario Modeling for Capital Reallocation

Forecasts only create value when they are tied to explicit decisions. Scenario modeling allows companies to test how different model inputs translate into different erosion curves and the associated trade-offs. Scenario modeling enables companies to explore questions such as:

- Which geographies remain economically defensible post-LoE?

- When do continued investments stop generating incremental returns?

- What post-LOE price strategy results in the best commercial outcome?

These insights ultimately help companies optimize capital allocation decisions and how to best redirect investments from low-potential LOE markets towards new or early-stage assets.

Leveraging ML to navigate decision-making around loss of exclusivity

Historically, LoE planning relied on a limited set of simplified assumptions: expected generic or biosimilar entry, an average erosion curve from a small set of previous analogues, and annual planning cycles. Those assumptions were imperfect, but no better alternatives existed.

In today’s heterogeneous environment, this assumption-based approach breaks down.

Erosion varies significantly based on:

- Market-specific Gx / BSM substitution rules

- Channel dynamics

- Product characteristics

- Disease area dynamics & patient/prescriber behavior

- Competitive factors and pricing

ML-Based Forecasting as the New LoE Decision-Making Tool

Machine learning changes how LoE can be managed by moving beyond one-off, assumption-driven projections toward data-driven, adaptive forecasting. Rather than relying on a small set of manually selected analogues and their past erosion curves, ML-based models learn from thousands of analogue characteristics across hundreds of assets and markets based on e.g., IQVIA Midas data.

In practice these ML-based models can:

- Learn from past LOE erosion observations - across therapy areas, products and markets

- Account for both product and market-specific characteristics and learn from thousands of different feature combinations to accurately develop a unique erosion prediction for the target being forecasted

- Dynamically update forecasts as new competitors enter or other market conditions change

- Provide insights on the most influential features for a given erosion forecast – allowing decision-makers to see whether e.g., price, commercial activity, Gx/BSM manufacturer historical aggressiveness, or market substitution enforcement is the most influential factor driving expectations

These models can be used to generate predictions for different strategic scenarios – e.g., allowing users to input different pricing scenarios and using that to predict expected volume. Additionally, they rely on no human assumptions as they automatically re-calculate product and market features based on objective data every month or quarter. These characteristics mean that leadership teams can be more agile and link forecasts directly to decisions on resource deployment, brand defense, and reinvestment timing.

In practice, this means that companies are better equipped to anticipate LOE impact and plan optimal strategic responses.

Scenario Modeling for Capital Reallocation

Forecasts only create value when they are tied to explicit decisions. Scenario modeling allows companies to test how different model inputs translate into different erosion curves and the associated trade-offs. Scenario modeling enables companies to explore questions such as:

- Which geographies remain economically defensible post-LoE?

- When do continued investments stop generating incremental returns?

- What post-LOE price strategy results in the best commercial outcome?

These insights ultimately help companies optimize capital allocation decisions and how to best redirect investments from low-potential LOE markets towards new or early-stage assets.

Leveraging ML to navigate decision-making around loss of exclusivity

Historically, LoE planning relied on a limited set of simplified assumptions: expected generic or biosimilar entry, an average erosion curve from a small set of previous analogues, and annual planning cycles. Those assumptions were imperfect, but no better alternatives existed.

In today’s heterogeneous environment, this assumption-based approach breaks down.

Erosion varies significantly based on:

- Market-specific Gx / BSM substitution rules

- Channel dynamics

- Product characteristics

- Disease area dynamics & patient/prescriber behavior

- Competitive factors and pricing

ML-Based Forecasting as the New LoE Decision-Making Tool

Machine learning changes how LoE can be managed by moving beyond one-off, assumption-driven projections toward data-driven, adaptive forecasting. Rather than relying on a small set of manually selected analogues and their past erosion curves, ML-based models learn from thousands of analogue characteristics across hundreds of assets and markets based on e.g., IQVIA Midas data.

In practice these ML-based models can:

- Learn from past LOE erosion observations - across therapy areas, products and markets

- Account for both product and market-specific characteristics and learn from thousands of different feature combinations to accurately develop a unique erosion prediction for the target being forecasted

- Dynamically update forecasts as new competitors enter or other market conditions change

- Provide insights on the most influential features for a given erosion forecast – allowing decision-makers to see whether e.g., price, commercial activity, Gx/BSM manufacturer historical aggressiveness, or market substitution enforcement is the most influential factor driving expectations

These models can be used to generate predictions for different strategic scenarios – e.g., allowing users to input different pricing scenarios and using that to predict expected volume. Additionally, they rely on no human assumptions as they automatically re-calculate product and market features based on objective data every month or quarter. These characteristics mean that leadership teams can be more agile and link forecasts directly to decisions on resource deployment, brand defense, and reinvestment timing.

In practice, this means that companies are better equipped to anticipate LOE impact and plan optimal strategic responses.

Scenario Modeling for Capital Reallocation

Forecasts only create value when they are tied to explicit decisions. Scenario modeling allows companies to test how different model inputs translate into different erosion curves and the associated trade-offs. Scenario modeling enables companies to explore questions such as:

- Which geographies remain economically defensible post-LoE?

- When do continued investments stop generating incremental returns?

- What post-LOE price strategy results in the best commercial outcome?

These insights ultimately help companies optimize capital allocation decisions and how to best redirect investments from low-potential LOE markets towards new or early-stage assets.

Leveraging ML to navigate decision-making around loss of exclusivity

Today’s launch environment is defined by a sustained cadence of launches. Many large life science companies are preparing multiple product launches each year, even as the peak revenue potential of most new assets has declined relative to prior decades. Industry analyses show that around half of recent launches underperform expectations, not because of insufficient clinical value, but because opportunity sizing, sequencing, and execution are misaligned with market reality.

Most new assets are:

- Later-in-class

- Relevant for specific patient subgroups

- Highly sensitive to access, guideline and sequencing decisions

This reality demands fundamentally different launch models and capabilities.

ML-Driven Launch Forecasting and Early Course Correction

ML-based launch forecasting approaches also represent a shift away from highly assumption-driven uptake predictions to a data-driven and adaptive alternative. Based on a similar dataset as for LOE predictions [e.g., IQVIA Midas data], the ML-model gets insights on hundreds of past launch uptake curves and product - and market characteristics for each of these. Correlating characteristics with observed past launch uptake, allows the ML model to develop accurate predictions for new assets.

ML-based launch forecasting enables companies to:

- Learn from characteristics of hundreds of past launches to form uptake predictions

- Continuously update uptake expectations using early market signals

- Identify which segments, geographies, or indications are over- or under-performing

- Reallocate resources while the launch is still in flight

In fragmented markets, speed of forecast correction becomes a competitive advantage.

Precision Resource Allocation

As opportunities become more targeted, resources must follow opportunity density. Predictive models allow teams to size field forces, prioritize markets, and sequence investments based on where adoption is most likely - and to adjust dynamically as reality unfolds.

Today’s launch environment is defined by a sustained cadence of launches. Many large life science companies are preparing multiple product launches each year, even as the peak revenue potential of most new assets has declined relative to prior decades. Industry analyses show that around half of recent launches underperform expectations, not because of insufficient clinical value, but because opportunity sizing, sequencing, and execution are misaligned with market reality.

Most new assets are:

- Later-in-class

- Relevant for specific patient subgroups

- Highly sensitive to access, guideline and sequencing decisions

This reality demands fundamentally different launch models and capabilities.

ML-Driven Launch Forecasting and Early Course Correction

ML-based launch forecasting approaches also represent a shift away from highly assumption-driven uptake predictions to a data-driven and adaptive alternative. Based on a similar dataset as for LOE predictions [e.g., IQVIA Midas data], the ML-model gets insights on hundreds of past launch uptake curves and product - and market characteristics for each of these. Correlating characteristics with observed past launch uptake, allows the ML model to develop accurate predictions for new assets.

ML-based launch forecasting enables companies to:

- Learn from characteristics of hundreds of past launches to form uptake predictions

- Continuously update uptake expectations using early market signals

- Identify which segments, geographies, or indications are over- or under-performing

- Reallocate resources while the launch is still in flight

In fragmented markets, speed of forecast correction becomes a competitive advantage.

Precision Resource Allocation

As opportunities become more targeted, resources must follow opportunity density. Predictive models allow teams to size field forces, prioritize markets, and sequence investments based on where adoption is most likely - and to adjust dynamically as reality unfolds.

Today’s launch environment is defined by a sustained cadence of launches. Many large life science companies are preparing multiple product launches each year, even as the peak revenue potential of most new assets has declined relative to prior decades. Industry analyses show that around half of recent launches underperform expectations, not because of insufficient clinical value, but because opportunity sizing, sequencing, and execution are misaligned with market reality.

Most new assets are:

- Later-in-class

- Relevant for specific patient subgroups

- Highly sensitive to access, guideline and sequencing decisions

This reality demands fundamentally different launch models and capabilities.

ML-Driven Launch Forecasting and Early Course Correction

ML-based launch forecasting approaches also represent a shift away from highly assumption-driven uptake predictions to a data-driven and adaptive alternative. Based on a similar dataset as for LOE predictions [e.g., IQVIA Midas data], the ML-model gets insights on hundreds of past launch uptake curves and product - and market characteristics for each of these. Correlating characteristics with observed past launch uptake, allows the ML model to develop accurate predictions for new assets.

ML-based launch forecasting enables companies to:

- Learn from characteristics of hundreds of past launches to form uptake predictions

- Continuously update uptake expectations using early market signals

- Identify which segments, geographies, or indications are over- or under-performing

- Reallocate resources while the launch is still in flight

In fragmented markets, speed of forecast correction becomes a competitive advantage.

Precision Resource Allocation

As opportunities become more targeted, resources must follow opportunity density. Predictive models allow teams to size field forces, prioritize markets, and sequence investments based on where adoption is most likely - and to adjust dynamically as reality unfolds.

Half of launches underperform. Speed of correction is the new edge.

Today’s launch environment is defined by a sustained cadence of launches. Many large life science companies are preparing multiple product launches each year, even as the peak revenue potential of most new assets has declined relative to prior decades. Industry analyses show that around half of recent launches underperform expectations, not because of insufficient clinical value, but because opportunity sizing, sequencing, and execution are misaligned with market reality.

Most new assets are:

- Later-in-class

- Relevant for specific patient subgroups

- Highly sensitive to access, guideline and sequencing decisions

This reality demands fundamentally different launch models and capabilities.

ML-Driven Launch Forecasting and Early Course Correction

ML-based launch forecasting approaches also represent a shift away from highly assumption-driven uptake predictions to a data-driven and adaptive alternative. Based on a similar dataset as for LOE predictions [e.g., IQVIA Midas data], the ML-model gets insights on hundreds of past launch uptake curves and product - and market characteristics for each of these. Correlating characteristics with observed past launch uptake, allows the ML model to develop accurate predictions for new assets.

ML-based launch forecasting enables companies to:

- Learn from characteristics of hundreds of past launches to form uptake predictions

- Continuously update uptake expectations using early market signals

- Identify which segments, geographies, or indications are over- or under-performing

- Reallocate resources while the launch is still in flight

In fragmented markets, speed of forecast correction becomes a competitive advantage.

Precision Resource Allocation

As opportunities become more targeted, resources must follow opportunity density. Predictive models allow teams to size field forces, prioritize markets, and sequence investments based on where adoption is most likely - and to adjust dynamically as reality unfolds.

Half of launches underperform. Speed of correction is the new edge.

Today’s launch environment is defined by a sustained cadence of launches. Many large life science companies are preparing multiple product launches each year, even as the peak revenue potential of most new assets has declined relative to prior decades. Industry analyses show that around half of recent launches underperform expectations, not because of insufficient clinical value, but because opportunity sizing, sequencing, and execution are misaligned with market reality.

Most new assets are:

- Later-in-class

- Relevant for specific patient subgroups

- Highly sensitive to access, guideline and sequencing decisions

This reality demands fundamentally different launch models and capabilities.

ML-Driven Launch Forecasting and Early Course Correction

ML-based launch forecasting approaches also represent a shift away from highly assumption-driven uptake predictions to a data-driven and adaptive alternative. Based on a similar dataset as for LOE predictions [e.g., IQVIA Midas data], the ML-model gets insights on hundreds of past launch uptake curves and product - and market characteristics for each of these. Correlating characteristics with observed past launch uptake, allows the ML model to develop accurate predictions for new assets.

ML-based launch forecasting enables companies to:

- Learn from characteristics of hundreds of past launches to form uptake predictions

- Continuously update uptake expectations using early market signals

- Identify which segments, geographies, or indications are over- or under-performing

- Reallocate resources while the launch is still in flight

In fragmented markets, speed of forecast correction becomes a competitive advantage.

Precision Resource Allocation

As opportunities become more targeted, resources must follow opportunity density. Predictive models allow teams to size field forces, prioritize markets, and sequence investments based on where adoption is most likely - and to adjust dynamically as reality unfolds.

Half of launches underperform. Speed of correction is the new edge.

Blockbusters have not disappeared - but the margin for forecasting error has collapsed. In this environment, success depends less on having perfect plans and more on building predictive systems that adapt faster than the market moves.

The winners will be those that embed prediction and scenario intelligence at the core of how they operate - across both the products they defend and the ones they bring to market.

Blockbusters have not disappeared - but the margin for forecasting error has collapsed. In this environment, success depends less on having perfect plans and more on building predictive systems that adapt faster than the market moves.

The winners will be those that embed prediction and scenario intelligence at the core of how they operate - across both the products they defend and the ones they bring to market.

Blockbusters have not disappeared - but the margin for forecasting error has collapsed. In this environment, success depends less on having perfect plans and more on building predictive systems that adapt faster than the market moves.

The winners will be those that embed prediction and scenario intelligence at the core of how they operate - across both the products they defend and the ones they bring to market.

Winners will adapt faster than the market moves

Blockbusters have not disappeared - but the margin for forecasting error has collapsed. In this environment, success depends less on having perfect plans and more on building predictive systems that adapt faster than the market moves.

The winners will be those that embed prediction and scenario intelligence at the core of how they operate - across both the products they defend and the ones they bring to market.

Winners will adapt faster than the market moves

Blockbusters have not disappeared - but the margin for forecasting error has collapsed. In this environment, success depends less on having perfect plans and more on building predictive systems that adapt faster than the market moves.

The winners will be those that embed prediction and scenario intelligence at the core of how they operate - across both the products they defend and the ones they bring to market.

Winners will adapt faster than the market moves

Clinical Decision Support tools are set to transform patient care - from tackling information overload and HCP shortages to enabling personalized, preventative healthcare. In this whitepaper, we explore how pharma and medtech can design, scale, and embed CDS solutions that create real clinical and commercial value. Sign up to receive the full whitepaper and get practical guidance for shaping the future of care.

.avif)

Are you planning to strengthen your forecasting capabilities?

Reach out if you'd like to explore how ML-based forecasting could work in your organization, want to discuss how to approach LoE planning or launch strategy under uncertainty, or are curious about what building this capability looks like in practice.

Sign up for the whitepaper and learn how Agentic AI is set to disrupt pharma’s commercial engagement - and why acting now is key to staying ahead. Explore how a strategic approach to AI adoption can help pharma scale impact, optimize operations, and unlock lasting value.

Click to read more

AI is revolutionizing the pharmaceutical industry, improving efficiency in drug discovery, clinical development, and customer engagement. Key applications like content creation, insights extraction, and predictive analytics streamline operations. To maximize AI’s potential, a strategic, holistic approach is crucial, avoiding siloed efforts and aligning with business goals for scalable success.

Click to read more

AI has the potential to revolutionize the pharmaceutical industry, but success hinges on selecting the right use cases. Without a structured approach, companies risk spreading resources too thin and missing out on scalable, impactful solutions. This article explores a strategic framework for evaluating and prioritizing AI projects, ensuring they align with corporate goals and deliver maximum value

Click to read more

Successfully implementing AI in pharma requires building a strong foundation across people, processes, and platforms.Intellishore’s approach involves assessing organizational readiness, identifying maturity gaps, and creating a roadmap to address these challenges. By focusing on targeted initiatives, organizations can enable AI innovation and achieve sustainable, long-term success.

Click to read more